What is a Liquidator in corporate accounting?

Corporate accounting is a specialist branch of accountancy that deals with the accounting for companies. A Liquidator in corporate matters will work closely with the accountant to advise and take action to rescue a business from insolvency or, if that’s not possible, close the company through liquidation.

The role of a Liquidator in corporate insolvency.

A Liquidator in corporate insolvency has to be a licensed insolvency practitioner. It’s their role to manage the liquidation process.

To give you an overview of ‘What is a Liquidator?’, their duties include:

- settling outstanding legal issues or contracts

- getting valuations for and selling off the company’s assets

- paying creditors with fund gained from the sale of assets

- handling the paperwork and liaise with relevant authorities

- paying all costs and final bills

- being the main contact for creditors

- interviewing the company’s directors to discover what went wrong with the business

- informing Companies House to have the company removed from its register.

A liquidator in corporate insolvency has a duty to get the best results for the creditors – not the directors.

What is a Liquidator when closing an insolvent company?

The most common way to close an insolvent company is using a Creditors’ Voluntary Liquidation (CVL), which is a formal liquidation process. The directors will instigate this process because the company cannot pay its debts now or in the future unless they release funds from the company through liquidation.

The first step is to call a shareholders’ meeting to seek approval for the liquidation. While the directors can – and should – consult a licensed insolvency practitioner before they call a shareholders’ meeting, appointing a licensed insolvency practitioner to act as Liquidator is done after approval is given.

To appoint a Liquidator in corporate CVL the directors can propose a licensed insolvency practitioner to use but they cannot secure their services without the agreement of the creditors.

A quick look at the CVL process

Step 1. Get shareholders’ approval. At least 75% of shareholders must agree to the liquidation.

Step 2. Appoint a Liquidator to take control of the CVL process.

Step 3. The Liquidator will send the winding-up resolution to Companies House. This has to be done within 15 days of the shareholders’ approval being given.

Step 4. The Liquidator investigates the reasons why insolvency has occurred

Step 5. The Liquidator gets valuation for the company’s assets and arranges for their sale.

Step 6. The Liquidator uses funds from the sale of assets to pay back outstanding debts.

Step 7. The Liquidator must send a notice of the liquidation to The Gazette, the official public record containing details of every company going through an insolvency process.

What is a Liquidator in a Compulsory Liquidation?

The Liquidator in corporate insolvency where a Compulsory Liquidation has been approved is appointed not by the company or creditors, but by the courts. The Liquidator is called ‘the official receiver’ but their role is the same as a Liquidator in corporate insolvency where a CVL is used: to liquidate the company and sell its assets to pay back the creditors. The directors of the company being liquidated often employ their own licensed insolvency practitioner to work alongside the court-appointed Liquidator.

What is a Liquidator when closing a solvent business?

If a company is solvent when it closes, using a Members’ Voluntary Liquidation (MVL) is the most tax efficient to do this.

The first step is to appoint a licensed insolvency practitioner to act as Liquidator. They will oversee the whole MVL process and wind up the company.

To get started, the Liquidator will draft a Declaration of Solvency that includes

- The name and address of the company and the company’s directors

- A statement of the company’s assets and liabilities

- A timeline of when the company will pay its debts

This is then signed with a solicitor or notary as witness.

Within five weeks of this declaration being signed, a general meeting of shareholders must be held, to pass a resolution for the voluntary liquidation.

As well as liquidating the company’s assets, taking care of paying outstanding bills and distributing the remaining funds to shareholders, the Liquidator will advertise the resolution in The Gazette and send the signed declaration to Companies House. The company will then be ‘struck off’ the Companies House register.

FAQs

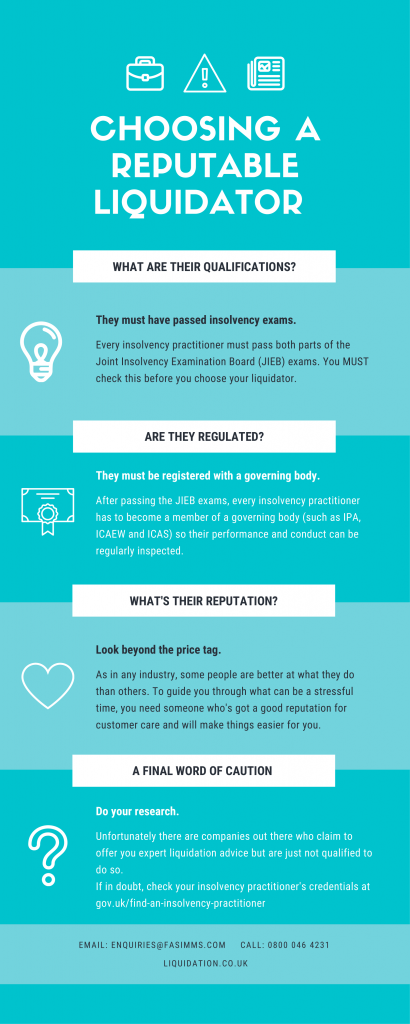

What’s the difference between the roles of the liquidator in corporate liquidation and the accountant?

An accountant will most likely have a good understanding of solvent and insolvent liquidation and be able to give an overview of some of liquidation options. They will also be able to provide the details of some reputable licensed insolvency practitioners to act as Liquidator.

A Liquidator has to have specialist training and qualifications to enable them to give the right advice for the company’s situation. All liquidation processes must be managed by a licensed insolvency practitioner, acting as Liquidator. An accountant cannot, by law, take any company through a liquidation process.

What’s the difference between a CVL and an MVL?

A CVL, Creditors’ Voluntary Liquidation, is a liquidation process used by a liquidator in corporate insolvency cases. If a company is insolvent it means it cannot meet its financial obligations.

An MVL, Members’ Voluntary Liquidation, is a liquidation process for solvent companies, which means the company has enough money to pay any outstanding debts.

Why do companies choose liquidation?

If the company is insolvent and can’t pay its debts, the directors might choose to close the company and sell its assets in order to cover some or all of these debts. Using a liquidation process like a CVL will also stop legal action being taken by creditors and ensure employees receive any outstanding monies owed to them.

For solvent companies, liquidation using an MVL is often a tax efficient way of closing a company. Contractors moving to employment can potentially get Business Asset Disposal Relief, which reduces the tax rate down to 10%. Retiring business owners, or those closing a dormant company, can receive tax benefits if they have available profits of over £25,000.

A Liquidator in corporate closures is a must. A company cannot go through an insolvent or solvent liquidation without a Liquidator’s services.

What is a liquidator looking for when they investigate why the insolvency occurred?

A liquidator in corporate insolvency will take charge of the company, once they are appointed, but the directors are legally obliged to cooperate with the Liquidator. From this point, the Liquidator has the power to sell the company’s assets, make payments to creditors and investigate all previous actions by the directors, to determine why the company failed.

They are looking for evidence of wrong-doing by the directors. This could be:

- Failing to keep proper or accurate company records

- Fraudulent trading

- Concealing assets or omitting assets from the company’s statement of affairs

- Misusing or appropriating company funds or assets for their own benefit

- Holding a director’s role while being a disqualified director

- Declarations of bankruptcy

- Committing any criminal offence that impacts the company

If they have enough evidence, the Liquidator is legally required to submit their findings. If there is a successful prosecution, the director or directors concerned can be disqualified from any management roles in a future company for a fixed period of time, face fines and possibly a prison sentence.

Review

There are no reviews yet. Be the first one to write one.